What do you do if you get laid off? What financial moves can you do to keep your head above water? What do you do next to bounce back? Laid off, reduction in force, terminated. It doesn't matter what term is used. It almost always hurts. Whether the layoff was expected or not, you still need to make smart money moves to avoid falling behind.

It can and has happened to all of us. Sometimes it's a result of issues with the company. Sometimes it can happen because of broader forces in the economy.

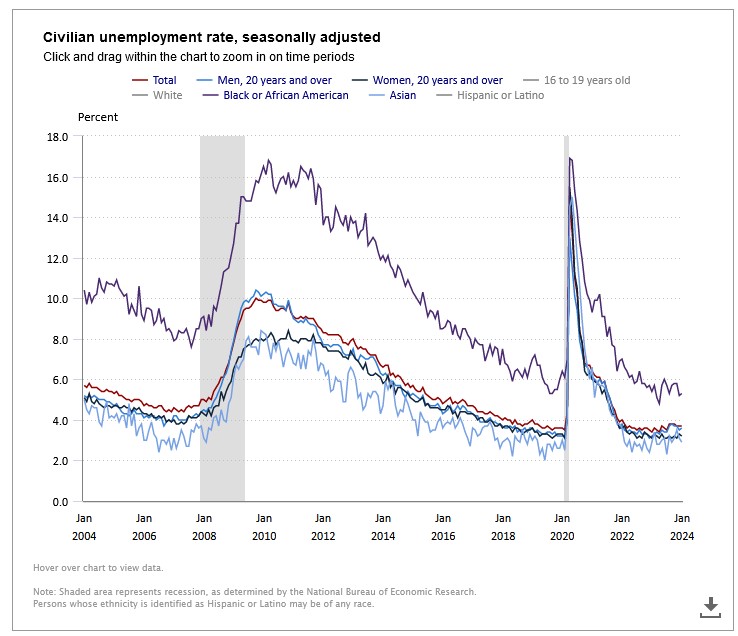

There's an old saw: Recession is when your neighbor loses his job. Depression is when you lose yours. And it can happen at any point in the business cycle. Right now, the US economy is in "full employment" mode. According to the US Department of Labor, the overall unemployment stands at about 3.7%, which is about where it was in February 2019. This is a far cry from where it was during the COVID-19 era when it was over 15% of the workforce or 10% during the Great Financial Crisis peak in 2009.

Regardless of how or when it happens,you need to be prepared to deal with a layoff.

Here are some ways to deal with the next steps after any layoff.

Cash Flow

1.) Emergency Fund: In some cases, the company may signal layoffs are coming. If you have time to prepare, then review your expenses, cut what you can, and increase your emergency reserves before you lose your job. Regardless of whether you know about a layoff, you should target to save an emergency fund to cover at least three months of expenses.

2.) Flexible Spending Account: If you have a Flexible Spending Account (FSA), you should consider spending the money while still employed or while covered under COBRA for items you may need when unemployed.

3.) Workplace Benefits: Be sure to get copies of all benefit summaries and discuss with HR to confirm details of benefits, compensation, treatment of sick pay, personal time off, vacation days, or any severance package. If you have stock options, you'll want to confirm details of the type and dates of grants and vesting.

4.) Unemployment Benefits: You may be entitled to unemployment benefits depending on the terms of your termination. Benefits are determined based on your state of residency, your earnings record, and family status. You can get an estimate of benefits by visiting your state's unemployment insurance website.

5.) Budget: Even in the best of times, this word is disliked by most folks. Right now, though, you'll need to get a handle on your spending. You'll need to determine the "must have" items that you can't change in the near term (like your mortgage or rent and loan payments) and your "nice to have" but discretionary items (like club memberships, streaming services, hobbies, vacations, and dining out). You should review your credit card and bank statements for at least the last quarter. You may find services or subscriptions that you don't use regularly. Consider cutting these items first.

Assets & Debts:

6.) Creditors: Reach out to creditors, explain your situation, and ask to either lower interest rates, defer payments, accrue interest or otherwise change loan terms. If you carry credit card balances, consider finding 0% interest rate promotional deals. Transfer balances from higher interest rate cards to the 0% promotional cards but try to stay at or below 40% of the total credit line of the new card. You'll want to do this to help maintain your credit. It's important to make at least your minimum payments during this time on all loans and keep the "utilization rate" of credit cards at 40% so that your credit score won't be adversely affected. Remember, new employers will likely be pulling a credit report as part of your employment application process. What you DON'T want to do is accept any loan or credit card forgiveness because this will be counted as taxable income when you file your tax returns.

7.) 401k Loans: If you have an outstanding loan on your workplace retirement plan, you'll have to either pay back the loan by a due date set in your plan documents or pay taxes on this as income. For most plans, the due date is the due date of your tax return for the year you leave your employer. So, you'll need to plan ahead to find a way to either pay this loan back by tax filing date or be prepared to have funds to pay taxes on it.

8.) Roth IRAs: You may want to consider using any Roth IRA balances to supplement cash needs if you get desperate. At least the principal portion of what you contributed will not be subject to income taxes.

9.) Home Equity Line of Credit (HELOC): If you have a HELOC, you can consider this as a back-stop to supplement covering your "must have" items or other emergencies that may come up during your unemployment period (such as home or auto repairs). If you have capacity on your line, you might even consider using it to pay down a portion of any higher interest credit cards. Even though most HELOCs are tied to the Prime Rate which has gone up sharply as the Federal Reserve has increased rates, the single-digit HELOC rate will likely still be less than many retail store credit cards that are in double digits. If you don't have a HELOC before getting laid off, you won't be able to get one when you do. So, try to have one in place. And, if there are any rumblings about layoffs, consider reaching out to apply long before you get that pink slip.

10.) Unvested Stock Options: Review your equity plan documents to determine your vesting schedule of stock grants. Try to coordinate your departure with your vesting schedule.

11.) Vested Stock Options: If your departure occurs after unvested stock options become vested, then consider exercising these options. You'll want to use the exercised options to provide cash to supplement what you'll need to cover hour "must have" items as well as add to your emergency fund.

12.) Retirement Plans: Whatever you've accumulated in your employer-sponsored retirement plan, you'll want to consider rolling these funds over into your own personal IRAs. You'll likely have more choices at lower costs. And if you do this, consider opening a "rollover" IRA which will help you preserve the option to roll the funds back into any future employer's plan. You should also be aware that not all retirement accounts are created the same. So, if you have pre-tax money in your company plan, you don't want to roll that into your individual Roth IRA. If you do, you'll cause the pre-tax money to be "converted" to the post-tax Roth. This will trigger a tax on the amount of the retirement funds converted. When you're trying to conserve cash, you don't want to create an unforced error resulting in a nasty tax surprise that will drain your cash.